Question

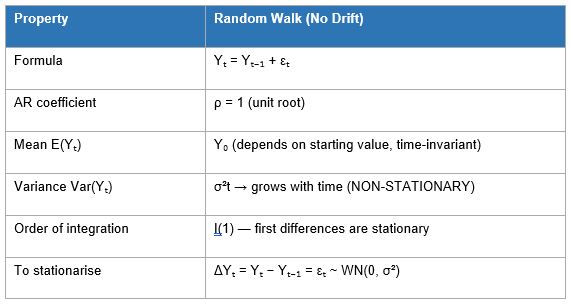

The equation of a random walk model WITHOUT drift is best represented as:

Option (A) = random walk WITH drift. Option (C) = trend-stationary (TS) process — fundamentally different from a unit root (DS) process. Option (D) = stationary AR(1).

Option (A) = random walk WITH drift. Option (C) = trend-stationary (TS) process — fundamentally different from a unit root (DS) process. Option (D) = stationary AR(1).More Research Questions

- If a Cobb-Douglas production is Q = K0.4 L0.6 the function is

- Match the development theories with their respective proponents. Column A: Theories 1. Theory of Unbalanced Growth 2. Theory of Critical Minimum Effort ...

- Which of the following is correct?

- The sum of squared deviation is minimum when taken from

- In a multiple regression model, if the inclusion of a new independent variable significantly changes the coefficient estimates of existing variables but is...

- Calculate Disposable income: Consumption (C) = 300 Investment (I) = 50 Government purchases (G) = 70 Government transfer payments (TP) = 15 Taxes (T) = 75 ...

- In the Harrod-Domar growth model, economic growth is determined by:

- Endogenity is associated with which of the following ?

- The H.M. and G.M. of a distribution are 8 and 10 respectively. Then the A.M. is

- What is the mean of a data if its Pearson's coefficient of skewness is 0.25, standard deviation is 6 and mode is 18

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt