Question

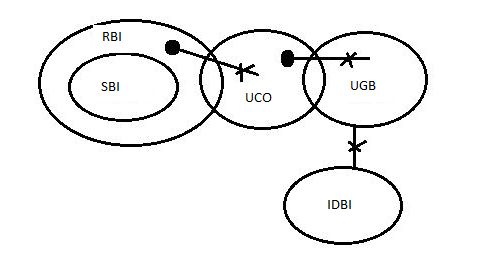

Statements : All SBI is RBI. Only a few RBI is UCO. Only a few UCO is UGB. No UGB is IDBI. Conclusions :

Statements : All SBI is RBI. Only a few RBI is UCO. Only a few UCO is UGB. No UGB is IDBI. Conclusions :

I. Some UCO not being UGB is a possibility.

II. Some SBI is UCO.

III. Some RBI being IDBI is a possibility.

In each of the questions below is given some statements followed by some conclusions. You have to take the given statements to be true even if they seem to be at variance with commonly known facts. Read all the conclusions and then decide which of the given conclusions logically follows from the given statements disregarding commonly known facts.

I. Some UCO not being UGB is a possibility that will not follow as some UCO are not UGB is already a definite conclusion. And we know that the possibility case of any conclusion that is definite does not follow. Hence conclusion I does not follow. II. Some SBI is UCO is not a definite conclusion. Hence conclusion II does not follow. III. Some RBI being IDBI is a possibilit y, There is no definite connection between RBI and IDBI so possible cases will follow, Hence conclusion III follows.

I. Some UCO not being UGB is a possibility that will not follow as some UCO are not UGB is already a definite conclusion. And we know that the possibility case of any conclusion that is definite does not follow. Hence conclusion I does not follow. II. Some SBI is UCO is not a definite conclusion. Hence conclusion II does not follow. III. Some RBI being IDBI is a possibilit y, There is no definite connection between RBI and IDBI so possible cases will follow, Hence conclusion III follows. More Syllogism Questions

- Statements: Only a few fan are lamp No fan is chair Only a few chair are lamp Conclusions: I. All chair can be lamp II. Some chair are not lamp

- Statements: Some Traditions are Creeds. All Creeds are Cultures. A few Cultures are Castes. No Value is a Caste. Conclusions: I. A few Traditions are Cultu...

- Two statements are given followed by three conclusions numbered I, II, and III assuming the statements to be true, even if they seem to be at variance with...

- Statements: All consonants are letters. All letters are noun. No noun is pronoun. Conclusions:I. All nouns are letters. II. All...

- Statements: Some bats are balls All balls are stumps Conclusions: I. Some stumps are bats II. Some bats are stumps

- Read the given statements and conclusions carefully. Assuming that the information given in the statements is true, even if it appears to be at variance wi...

- Statements: No Pencil is a Sharpener. Only a few Sharpeners are Erasers. 98% of Erasers are Pens. 100% Pens are Boxes. Conclusions: I. Some Boxes are Pens ...

- In the questions given below, there are three statements followed by three conclusions I, II and III. You have to take the three given statements to be tru...

- In each question below are given three statements followed by three conclusions numbered I, II and III. You have to take the two given statements to be tru...

- Three statements are followed by four conclusions numbered I, II, III, and IV. You have to consider these statements to be true, even if they seem at varia...

Relevant for Exams:

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt