Question

When the auditor, having obtained sufficient appropriate audit evidence, concludes that misstatements, individually or in aggregate, are both material and pervasive to the financial statements, he/she shall express which type of audit opinion?

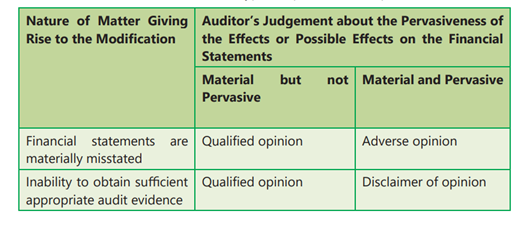

Read the following passage and answer the next 4 question (Q23-Q26) The purpose of an audit is to enhance the degree of confidence of intended users of the financial statements. The aforesaid purpose is achieved by the expression of an independent reporting by the auditor as to whether the financial statements exhibit a true and fair view of the affairs of the entity. Thus, an audit report is an opinion drawn on the entity’s financial statements to make sure that the records are true and fair representation of the transactions they claim to represent. This involves considering whether the financial statements have been prepared in accordance with an acceptable financial reporting framework applicable to the entity under audit. It is also necessary to consider whether the financial statements comply with the relevant statutory requirements. The main users of audit report are shareholders, members and all other stakeholders of the company. SA 700 (Revised) - “Forming an Opinion and Reporting on Financial Statements”, deals with the auditor’s responsibility to form an opinion on the financial statements. It also deals with the form and content of the auditor’s report issued as a result of an audit of financial statements

More Banking System in India Questions

- Champion Ltd. define following data for calculating Current Ratio: Current Assets Rs.20,00,000 , Inventories Rs.10,00,000 , Working Capital Rs.12, 00,000.

- As per the Union Budget 2023 announcements, Extension of tax benefit period for relocation of AIFs (Alternate Investment Fund) to new find location in GIFT...

- According to the IFSCA (BATF) Regulations 2024, how much office space must a BATF Service Provider allocate per employee in t he IFSC?

- Which statement is true out of the following with regards to technical analysis:

- The Reserve Bank of India, recently has proposed to hike UPI (Unified Payment Interface) transaction limit for investing in IPO to………………….

- With reference to the NBFCs, consider the following statements: 1. It is a company registered under the Companies Act, 1956 2. NBFC cannot accept demand de...

- What does the term "capital structure" refer to in the context of corporate finance?

- Which of the following cities is ranked second in the Global Financial Centres Index 35 (GFCI 35)?

- Firm's Cost of Capital is the average cost of:

- Under Priority 2 of the Union Budget 2024-25, which of is designed to incentivize job creation in the manufacturing sector?

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt