Question

Which of the following statement(s) about NBFCs is incorrect?

Read the following passage and answer the next 4 questions Reserve Bank of India has been regulating the financial activities of the Non-Banking Financial Companies under the provisions of Chapter III B of the Reserve Bank of India Act, 1934. With the amendment of the Reserve Bank of India Act, 1934 in January 1997, in terms of Section 45 IA of the said Act, and amendment of the National Housing Bank Act, 1987 in August 2019, in terms of Section 29 A of the National Housing Bank Act, 1987, all Non-Banking Financial Companies including Housing Finance Companies have to be mandatorily registered with the Reserve Bank of India. The credit-related matters of banks have been progressively deregulated by the Reserve Bank of India. Consistent with the policy of bestowing greater operational freedom to banks in the matter of credit dispensation and in the context of mandatory registration of NBFCs with the Reserve Bank, most of the aspects relating to the financing of NBFCs by banks have also been deregulated

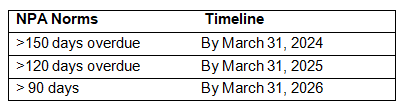

The glide path will not be applicable to NBFCs which are already required to follow the 90-day NPA norm. · There shall be a ceiling of Rs.1 crore per borrower for financing subscription to Initial Public Offer (IPO). NBFCs can fix more conservative limits. Please refer to the Circular RBI/2021-22/112 DOR.CRE.REC.No.60/03.10.001/2021-22 dated 12.10.2021 for more details (also refer to notes on NBFCs)

The glide path will not be applicable to NBFCs which are already required to follow the 90-day NPA norm. · There shall be a ceiling of Rs.1 crore per borrower for financing subscription to Initial Public Offer (IPO). NBFCs can fix more conservative limits. Please refer to the Circular RBI/2021-22/112 DOR.CRE.REC.No.60/03.10.001/2021-22 dated 12.10.2021 for more details (also refer to notes on NBFCs) More Banking System in India Questions

- According to the guidelines on the India-UAE Comprehensive Economic Partnership Agreement (CEPA), which entity is responsible for overseeing the import of ...

- How many Post Offices will be on-boarded Core Banking System as per Union Budget 2022-23?

- Under the regulation of which act can scheduled commercial bank take equity stake in a payments bank to the extent permitted?

- The elements given below are some of the parts of the M4 money supply of Indian economy (a) Broad money (M3) (b) All deposits with the post office savi...

- Which of the following are common barriers to achieving financial inclusion? 1) Lack of physical infrastructure, such as bank branches and ATMs, in remote...

- Accounting policy for inventories of Xeta Enterprises states that inventories are valued at the lower of cost determined on weighted average basis or net r...

- What is the group borrower exposure limit for an NBFC-IFC in the middle layer as per the scale-based regulations (SBR) for NBFCs?

- Consider the following statement: I. Highest surcharge rate on income above 5 crore to be reduced from 37% to 30% under new regime II. Extending benefits o...

- What type of a merger refers to two firms operating in same industry or producing identical products combining together?

- How must entities with multiple lines of business (LoBs) granted by IFSCA complete their registration on the FIU-IND FINNET 2.0 Portal as per the March 202...

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt