Question

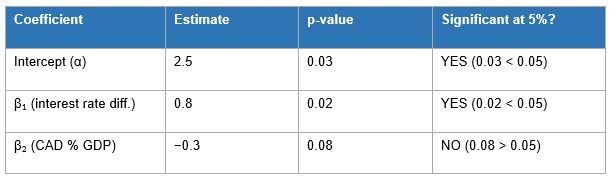

A regression equation from an Indian bank: Ŷ = 2.5 + 0.8X₁ − 0.3X₂. p-values: α̂: 0.03, β̂₁: 0.02, β̂₂: 0.08. At 5% significance level, which is correct?

We cannot confidently reject H₀: β₂ = 0. Option (C) confuses economic significance with statistical significance. Option (D) is risky — dropping a relevant variable causes omitted variable bias.

We cannot confidently reject H₀: β₂ = 0. Option (C) confuses economic significance with statistical significance. Option (D) is risky — dropping a relevant variable causes omitted variable bias.More Research Questions

- If the money supply grows 5 per cent, and real output grows 2 per cent, prices should rise by

- For which of the following consumption functions, the value of income multiplier, k=4?

- The equation for a supply curve is P = 3Q – 8. What is the elasticity in moving from a price of 4 to a price of 7?

- In a market economy

- When a firm operates with excess capacity

- In case of Multicollinearity, if the Ri2(Coefficient of auxiliary regression on independent variables) is 0.80 and the variance of the OLS estimator is 1.5...

- If bxy = 0.20 and rxy = 0.50, then byx is equal to:

- An oil exploration company intends to drill an exploratory well in each of two geologically unrelated regions A and B. If the probability of finding oil in...

- The Travel Cost Method (TCM) is a Revealed Preference Method. What type of environmental good or service is it typically used to value, and what actual con...

- For the following demand curve, Q=10P-2 , calculate the profit made by the monopolist when Marginal cost is Rs.2

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt