Question

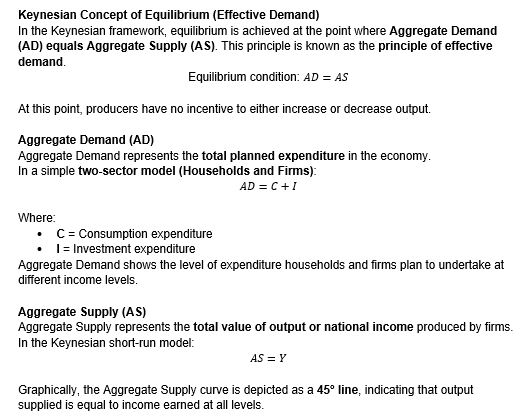

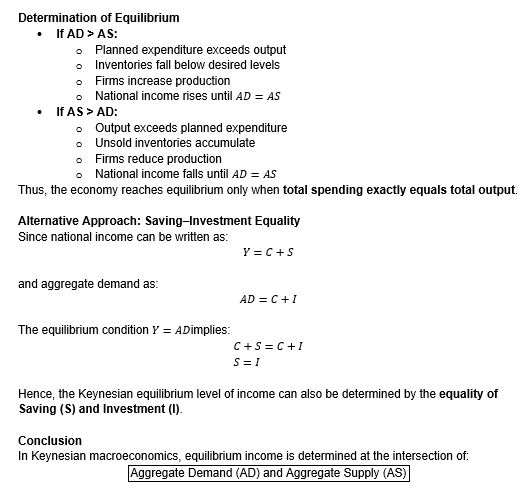

According to Keynesian theory, the equilibrium level of income and output in an economy is determined by the intersection of:

Both the AD–AS approach and the Saving–Investment approach lead to the same equilibrium level of national income.

Both the AD–AS approach and the Saving–Investment approach lead to the same equilibrium level of national income. More Research Questions

- CBDC concern for monetary policy transmission:

- What is the target Fiscal Deficit as a % of GDP for FY23 in the Union Budget 2022-23?

- If the endowment of some resource increases, the industry that uses that resource most intensively will increase its output while the other industry will d...

- According to the Quantity Theory of Money (QTM), what is the effect of a change in the velocity of money on the price level in the long run?

- Let X and Y represent prices in Rs of a commodity in Kolkata and Mumbai respectively. It is given X(bar) = 65, Y(bar) = 67, standard deviation of X = 2.5, ...

- Under Perfect Competition, Consider X’s production function to be Q=(min{K,L})1/2 , the price of capital is Rs.2 and price of labor is Rs.1. Calculate the ...

- For the demand function Q=a-P and the Marginal cost = c. Arrange the quantity produced by the following models in ascending order I) Bertnard II) Mon...

- In the classical IS-LM framework with a vertical LM curve, the government increases expenditure financed by bond issuance. Which of the following outcomes ...

- When the expected future marginal product of capital increases, then the IS curve

- Which of the following statements about a firm's average cost curves is false?

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt