Question

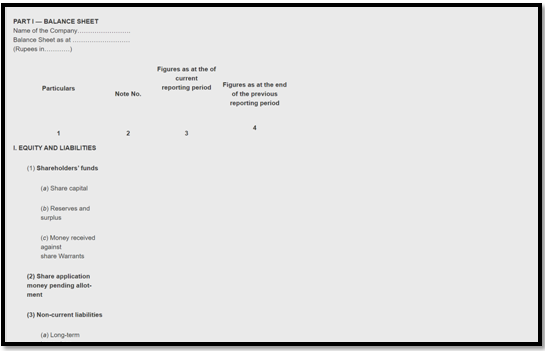

Divyam Textiles ltd has received money against share warrants which will be converted into shares after 2 years at rate of 1:2. The money so received, will be shown in the Balance sheet under ________

More Banking System in India Questions

- Calculate Debt ‐ Equity

- In the case of_____, either outflow of resources to settle the obligation is not probable or the amount expected to be paid to settle the liability cannot ...

- A and B exchange currency at a rate that takes place after a period of 1 month from spot date. What is the rate called in such case?

- Find the false statement with respect to Atal Pension Yojana.

- Which of the following statement(s) about NBFCs is incorrect?

- Which of the following are used by RBI as key measure of inflation?

- When was the Securities and Exchange Board of India enacted?

- Which of the following is NOT a monetary policy tool used by RBI?

- In which of the following years, India took its first major step towards liberalisation?

- The RBI’s guidelines on the formation of new districts in Madhya Pradesh, issued in January 2024, designated which bank as the Lead Bank for the newly form...

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt