Question

Which of the following is not a type of modified opinion?

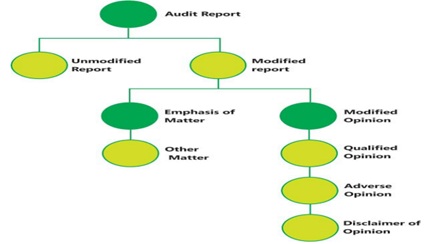

Read the following passage and answer the next 4 question (Q23-Q26) The purpose of an audit is to enhance the degree of confidence of intended users of the financial statements. The aforesaid purpose is achieved by the expression of an independent reporting by the auditor as to whether the financial statements exhibit a true and fair view of the affairs of the entity. Thus, an audit report is an opinion drawn on the entity’s financial statements to make sure that the records are true and fair representation of the transactions they claim to represent. This involves considering whether the financial statements have been prepared in accordance with an acceptable financial reporting framework applicable to the entity under audit. It is also necessary to consider whether the financial statements comply with the relevant statutory requirements. The main users of audit report are shareholders, members and all other stakeholders of the company. SA 700 (Revised) - “Forming an Opinion and Reporting on Financial Statements”, deals with the auditor’s responsibility to form an opinion on the financial statements. It also deals with the form and content of the auditor’s report issued as a result of an audit of financial statements

More Alternate Sources of Finance Questions

- What is Interoperability in connection with trades executed at Stock Exchanges?

- Which of the following is not a tool of financial statement analysis?

- As per Union Budget 2025-26, w hat is the new deadline for investments by Sovereign Wealth Funds and Pension Funds in the infrastructure sector?

- What is the primary purpose of integrity in ethical behavior?

- What are the needs listed in Maslow's pyramid from bottom to top?

- How many stressed accounts have been identified for transfer to NARCL (National Asset Reconstruction Company Limited) in a phased manner initially

- Subscribers to the Minimum Assured Return Scheme (MARS) under the new pension system (NPS) will have to stay invested for how many years to claim the guara...

- Conscientiousness measures what aspect of a person's personality?

- What is a key consideration when writing a report?

- A company fails to accrue wages for March that will be paid in April. The company’s year-end balance sheet liabilities:

Hey! Ask a query

Please enter email id

The email must be a valid email address.

Please enter Mobile Number

Please enter valid Mobile Number

Please enter your Doubt